This section lays out the requirements for the mitigation activities which are required outside of the organizational value chain. Specifically, the requirements of the use of carbon credits to reach the carbon neutral position of the subject.

The organization must compensate and/or neutralize the required emissions sources measured as a minimum, but are highly encouraged to go beyond the required emissions sources and include additional emissions categories. Organizations should consider the expectations of their stakeholders when deciding which additional emissions sources and categories should be compensated.

Purpose

This section specifies the criteria for use of environmental instruments in CarbonNeutral certifications and which instruments meet the criteria.

4.2.1.1 Carbon credits

Criteria

All carbon credits used towards the achievement of CarbonNeutral® certification must meet the following criteria:

Additional: An emission reduction project is said to be additional when it can be demonstrated that in the absence of the availability of carbon finance the project activity would not have occurred (the “baseline” scenario); and, such baseline scenario would have resulted in higher GHG emissions. Each eligible carbon accounting standard under The CarbonNeutral Protocol provides tools for how additionality at a project level is tested and demonstrated. For further discussion of this topic, see Guidance 4.5.

Legally attributable: Carbon credits must have a clear record of ownership from project owner and thereafter.

Measurable: Emissions reductions are quantified relative to a transparent and robust baseline scenario using recognized, peer-reviewed, published methods and project-specific data; or, using recognized performance standard procedures.

Permanent: Emissions reductions are permanent. Where reductions are generated by projects that carry risk of reversal, adequate safeguards must be in place to ensure that the risk of reversal is minimized and that, if any reversal occurs, a mechanism is in place that guarantees the reductions will be replaced.

Unique: Emissions reductions are held and retired on a registry to ensure that no more than one carbon credit can be associated with a single emission reduction.

Independently verified: Emissions reductions are verified by an expert third party qualified to verify carbon credits to ensure the criteria above have been met.

Further considerations

Emission reduction projects have impacts in addition to GHG emission reductions. While many projects have positive co-benefits, some may have negative impacts. Carbon credit standards accepted by The CarbonNeutral Protocol have requirements that material negative impacts should not arise from emission reduction projects.

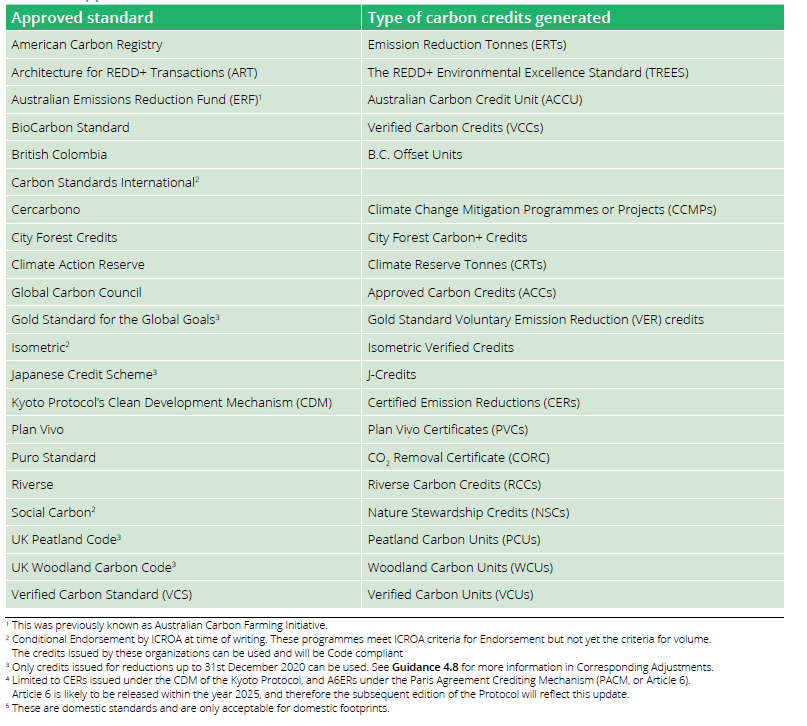

Approved carbon credit standards and project types

Carbon credits verified under the standards set forth in Table 10 are considered appropriate for use in corporate carbon neutrality programs as they have been determined to be additional, legally attributable, measurable, permanent, unique and independently verified, and therefore are qualified for use as external environmental instruments to reduce a subject’s GHG emissions. This list of standards is reviewed annually and updated from time to time to reflect developments in best practice and the performance of carbon credit standards.

In general, any mitigation project recognized under the standards is accepted under the Protocol, and carbon credits are treated equally across standards, vintage and project types. There are exceptions to this general approach, as set out below which identifies projects types that are not accepted under the Protocol and the reasons for the exclusions.

Consideration of the Core Carbon Principles

The Integrity Council for the Voluntary Carbon Market (ICVCM) published its Core Carbon Principles (CCPs) in March 2023. The ICVCM assesses carbon-crediting programs and methodology types against the CCPs, with the intention that CCP-labelled carbon credits will bring integrity to the market. The ICVCM commenced its assessment phase for carbon crediting programmes in late 2023, and for carbon credit methodologies in 2024.

At the time of publication for this 2025 Protocol, the ICVCM has released the assessment results of a limited number of project methodologies. CCP-labelled credits are not yet widely available, and are likely to be limited in availability in the near term.

The Protocol acknowledges the important role of the ICVCM and CCPs in the continued evolution of high-quality carbon credits. However, in the interim, as the supply of CCP-approved credits scales up in the market, organizations may use carbon credits verified under the standards set forth in Table 10 and in line with the Protocol’s criteria - legally attributable, measurable, permanent, unique and independently verified. The Protocol will consider the further role of any quality label markers for certification in the future, including whether CCP-labelled credits should be a mandatory requirement.

Exceptions

If the carbon credits from these standards are not in accordance with all of the criteria covering carbon credits - legally attributable, measurable, permanent, unique and independently verified—they must not be used for offsetting. As a consequence, Forward Mitigation Units from CAR, ex-ante forestry credits under the Gold Standard, Pending Issuance Units (PIUs) under the UK Woodland and Peatland code and t-CERs and l-CERs under the CDM are not acceptable.

Removal carbon credits

The Protocol treats mitigation projects that avoid and reduce emissions and those that remove GHGs from the atmosphere as equal. The logic underpinning this approach is the ‘overflowing bath-tub’ analogy. With the taps on, a balance is achieved either by turning down the taps (avoid or reduce emissions) or by draining an equal amount down the plug (removing emissions from the atmosphere and capturing them in carbon sinks). Both approaches have a critical role to play in mitigating climate change. However, as we get closer and closer to the safe limit of GHG concentrations in the atmosphere, clients should consider an increasing role for removal projects.

Excluded project types

Due to historic concerns on quality, the following project types must not be used towards the achievement of CarbonNeutral® certification, although they are recognized under some carbon credit standards in Table 10:

Under the provisions of the GHG Protocol Scope 2 Guidance, entities may purchase and retire EACs to support a zero emission grid factor for Scope 2 emissions. For non-owned renewable energy consumption, EACs are the most credible evidence of energy compensation, and claims without EACs in geographies where they are available are questionable/ potentially problematic (1).However, as the GHG Protocol is a respected third-party carbon accounting standard, its Scope 2 guidance is accepted under The CarbonNeutral Protocol.

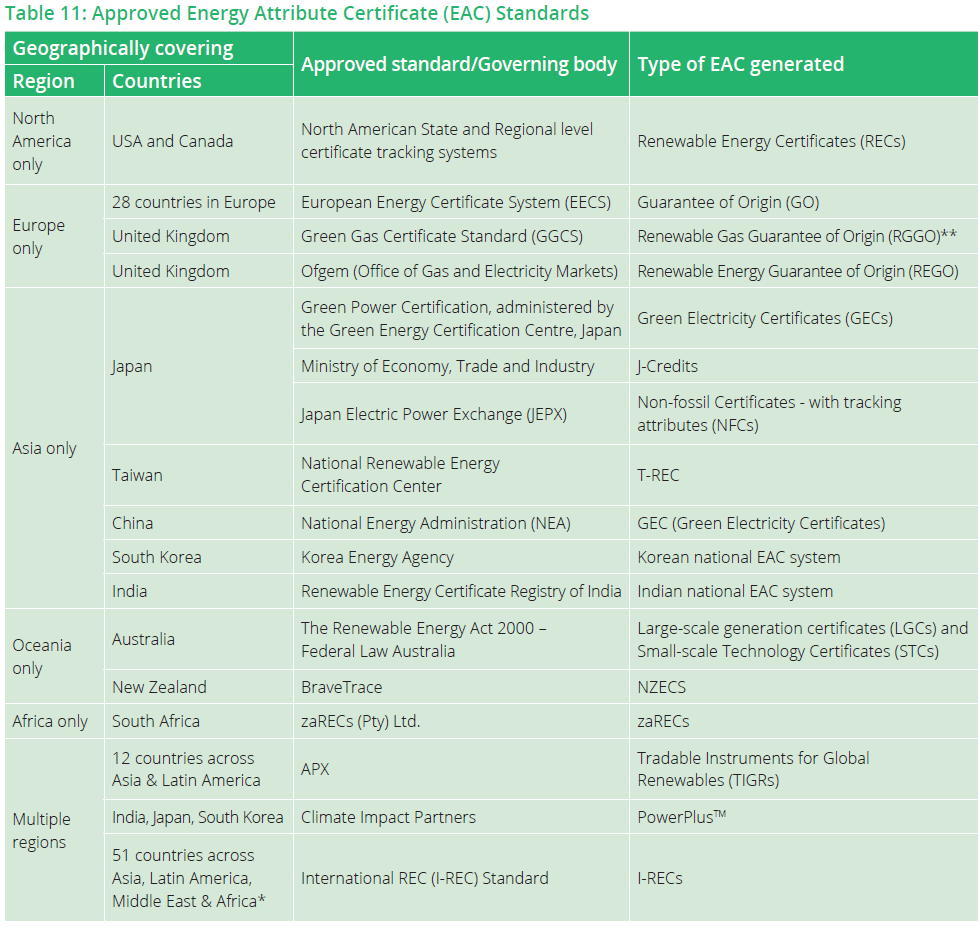

Table 11 lists the EAC standards that are acceptable for a Scope 2 or Scope 1 claim within a CarbonNeutral program that follows the market-based GHG accounting approach defined by the GHG Protocol Scope 2 Guidance. It is not an exhaustive list, rather it details those EACs in most common use within CarbonNeutral programs.

EAC programs generally prescribe applicable validity periods. In cases where validity periods are not prescribed, EACs issued within one year of the period covered by the CarbonNeutral® certification must be used.

Third-party certification and labelling of EACs

In some markets, a third party may also certify EACs based on an established standard that specifies a set of criteria which can be applied to determine which certificates can receive the label. The criteria used to define a subset of eligible EACs are typically based on technology or the commissioning date of the renewable energy facility.

Aligning procurement decisions with these criteria demonstrates impact that goes beyond the lowest-cost EAC solution. Examples of voluntary certification programs commonly used within CarbonNeutral programs include Green-e Energy in North America and EKOenergy, which is a global EAC label.

For guidance on EACs and Scope 3 emissions see Guidance 2.4.2 Treatment of Energy Attribute Certificates (EAC) in Scope 3 emissions. *I-REC Standard, accessed February 2024. **All EACs listed cover Scope 2 except Renewable Gas Guarantees of Origin (RGGO) which cover Scope 1.