The GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (also referred to as the Scope 3 Standard) developed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD) provides requirements and guidance for companies preparing and publicly reporting GHG emission inventories that include indirect emissions resulting from value chain activities (i.e. Scope 3 emissions). The Scope 3 Standard complements and builds upon the GHG Protocol Corporate Accounting and Reporting Standard to promote additional completeness and consistency in the way companies account for and report on

indirect emissions from value chain activities.

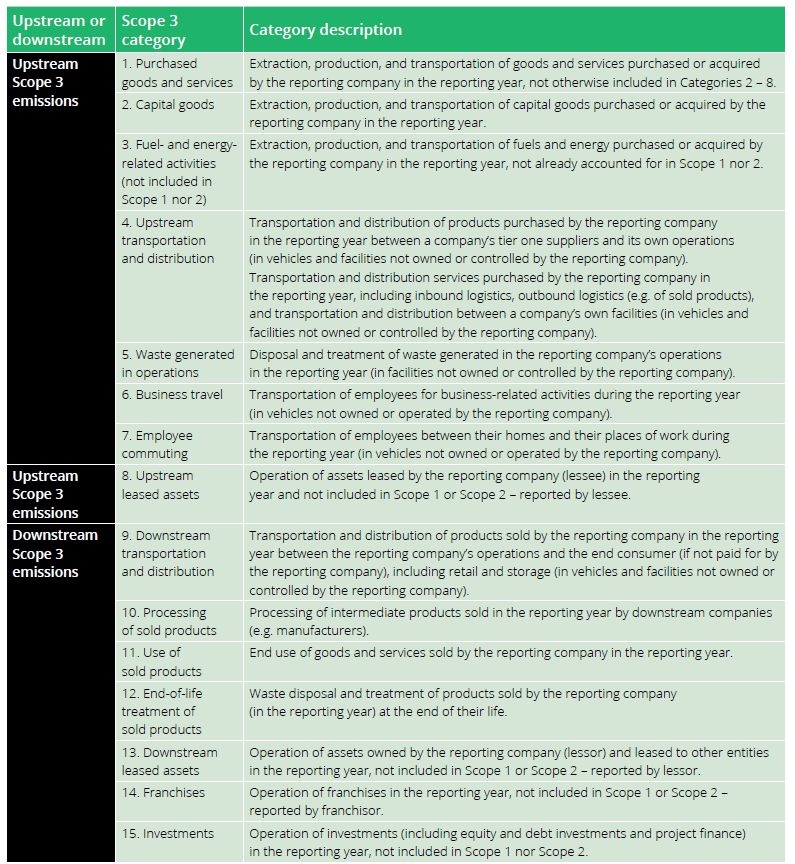

The Scope 3 Standard groups Scope 3 emissions into 15 distinct categories, as shown in Table 7. The categories are intended to provide companies with a systematic framework to organize, understand, and report on the diversity of Scope 3 activities within a corporate value chain.

For additional information about the GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard and its 15 Scope 3 categories refer to: www.ghgprotocol.org/standards/scope-3-standard

Image: Degraded Grasslands Afforestation, Uruguay: Using carbon finance, this project is implementing sustainable wood production, land restoration, and carbon sequestration through afforestation on degraded land in Uruguay.

*GHG Protocol, 2011, Corporate Value Chain (Scope 3) Accounting and Reporting Standard, https://ghgprotocol.org/standards/scope-3-standard.